Stop Googling the same numbers every year. Here is every important Canadian financial figure — contribution limits, tax brackets, deadlines, compound growth tables, and rules of thumb — on one page. Bookmark it. Print it. Send it to someone who needs it.

Registered Accounts (TFSA / RRSP / FHSA)

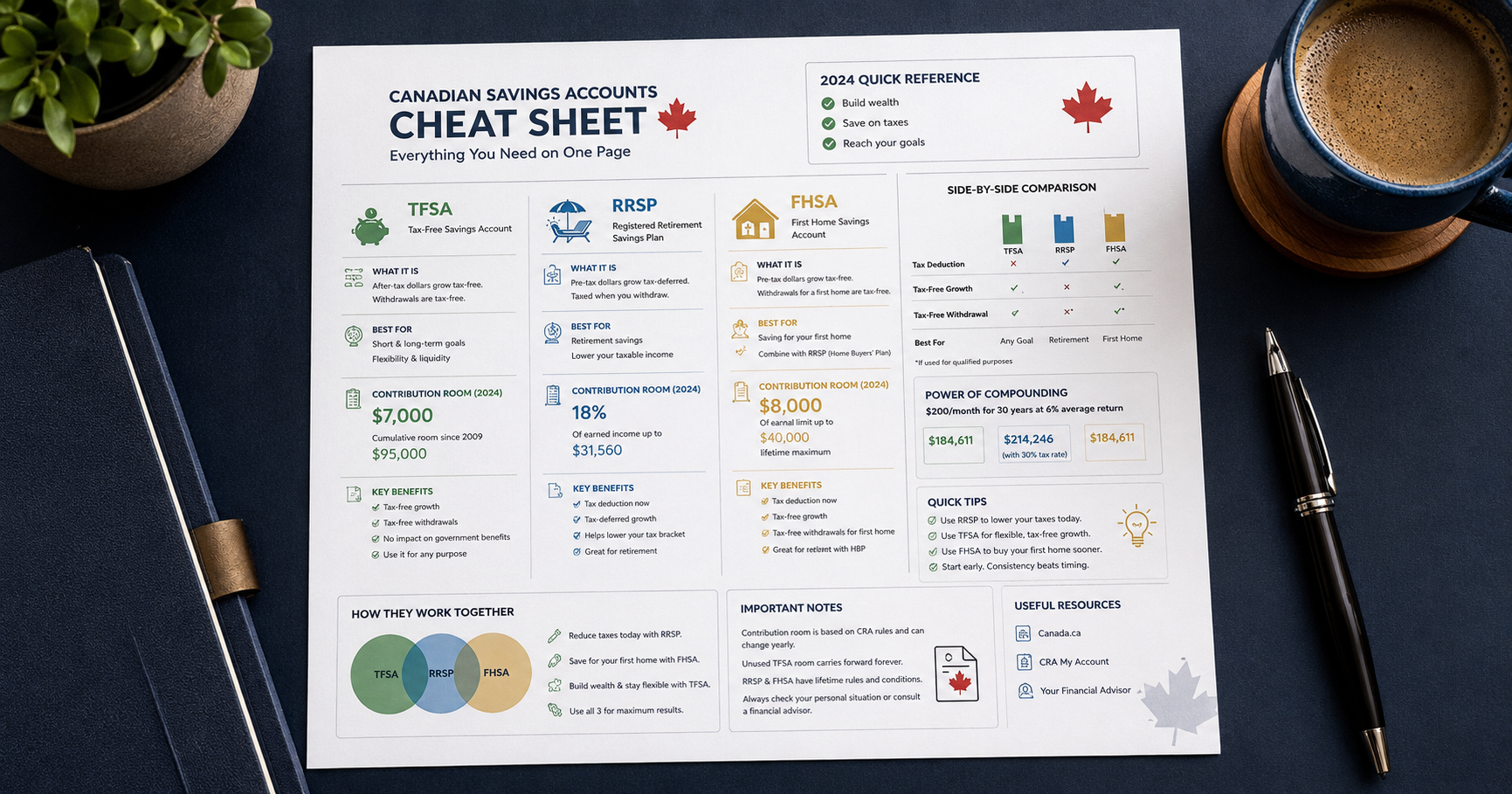

| TFSA | RRSP | FHSA | |

|---|---|---|---|

| 2026 Limit | $7,000 | 18% of income (max $32,490) | $8,000 |

| Lifetime Max | $102,000 (since 2009) | Based on income history | $40,000 |

| Tax deduction? | No | Yes | Yes |

| Tax-free growth? | Yes | Tax-deferred | Yes |

| Tax-free withdrawal? | Yes | No (taxed as income) | Yes (for first home) |

| Best for | Flexibility, any goal | High earners, retirement | First home purchase |

The FHSA is the only account with all three tax advantages simultaneously. If you do not own a home, it should be your first priority. Full FHSA breakdown here. For a detailed comparison of all three, see our TFSA vs RRSP vs FHSA guide.

2026 Federal Tax Brackets

| Taxable Income | Federal Rate | Tax on Max of Bracket |

|---|---|---|

| $0 to $57,375 | 15% | $8,606 |

| $57,375 to $114,750 | 20.5% | $11,762 |

| $114,750 to $159,222 | 26% | $11,563 |

| $159,222 to $221,708 | 29% | $18,121 |

| $221,708+ | 33% | -- |

The basic personal amount (the income you earn tax-free) is $16,129 for 2026. Remember: provincial tax is added on top of these federal rates.

Quick Tip

Your RRSP deduction is most valuable when your income is in a higher bracket. Contributing enough to drop from the 26% bracket to the 20.5% bracket saves you 26 cents per dollar contributed. At the 15% bracket, TFSA is usually better.

Key Financial Deadlines (2026)

| January 1 | New TFSA and FHSA contribution room begins |

| March 3 | RRSP contribution deadline (for 2025 tax year deduction) |

| March 15 | First quarterly tax installment due |

| April 30 | Tax filing deadline (individuals) |

| June 15 | Tax filing deadline (self-employed) |

| December 31 | Last day for TFSA/FHSA contributions for this year; RRSP final year at age 71 |

CPP and EI (2026)

| CPP max pensionable earnings | $71,300 |

| CPP employee contribution rate | 5.95% |

| CPP max employee contribution | $3,867 |

| EI max insurable earnings | $65,700 |

| EI premium rate (employee) | 1.64% |

| EI max annual premium | $1,077 |

If you are self-employed, you pay both the employee and employer portions of CPP (11.9% total). You do not pay EI unless you opt in.

What $500/Month Becomes (7% Average Return)

| Time | You Invest | It Becomes | Free Growth |

|---|---|---|---|

| 5 years | $30,000 | $35,800 | +$5,800 |

| 10 years | $60,000 | $86,500 | +$26,500 |

| 15 years | $90,000 | $158,400 | +$68,400 |

| 20 years | $120,000 | $260,500 | +$140,500 |

| 25 years | $150,000 | $405,200 | +$255,200 |

| 30 years | $180,000 | $610,000 | +$430,000 |

This is why starting early matters more than investing more later. Someone who invests $500/month from age 25 to 55 ends up with $610,000 — of which $430,000 is pure compound growth. Time is the variable that changes everything. Use your net worth calculator to see where you stand today.

The Power of Starting Now

Waiting 5 years to start costs you roughly $150,000 in final wealth (the difference between 30 years and 25 years of compounding). There is no amount of extra monthly contributions that efficiently makes up for lost time.

Rules of Thumb

| Emergency fund | 3-6 months of living expenses in cash |

| Housing costs | Maximum 30% of gross income |

| Savings rate target | 20% of take-home pay (minimum) |

| Retirement number | 25x your annual expenses (the 4% rule) |

| Debt payoff priority | Highest interest rate first (avalanche method) |

| Credit score | 680+ is good, 750+ is excellent |

| Net worth target (age 30) | ~1x your annual salary |

| Net worth target (age 40) | ~3x your annual salary |

These are guidelines, not laws. If your housing costs 35% of your income but you are saving 20% and debt-free, you are fine. Context matters more than rules. Use the debt payoff calculator if you are working on eliminating debt first.

The Priority Order

If you are wondering where your next dollar should go, here is the general order for most Canadians:

- Employer RRSP match — Free money. Always take it.

- High-interest debt — Kill anything above 7% interest.

- Emergency fund — 3 months minimum in a TFSA savings account.

- FHSA — $8,000/year if you do not own a home.

- TFSA — Max it ($7,000/year). Flexible and tax-free.

- RRSP — Fill remaining room if income is above $55K.

- Non-registered investing — After all registered accounts are maxed.

Adjust based on your situation. Someone with no debt and no home-buying plans skips straight to TFSA. Someone earning $120K prioritizes RRSP higher. The AI coaching tool can help you figure out your specific order.

Bookmark This Page

Financial numbers change every year. We update this cheat sheet annually with new contribution limits, tax brackets, and deadlines. Bookmark it and check back every January.

Need the full deep-dive on any of these topics? Start with the TFSA vs RRSP vs FHSA comparison, or check out all our free financial tools. For a complete wealth-building roadmap, read 47 Finance Tips for 2026.

Share this page with someone who needs it. Everyone deserves access to the numbers.

About Sarah Patel

Sarah specializes in helping businesses optimize their financial operations and make strategic investment decisions. Her background in both traditional finance and fintech gives her a unique perspective on modern business challenges.

More articles by this author